The safeguards put in place during the financial crisis of 2008 had a significant influence on the foreclosure process, establishing the framework for a healthier and more transparent relationship between the lender and the homeowner. When the global pandemic endangered homeowners' financial well-being, federal, state, and municipal governments and agencies and loan servicers and lenders worked tirelessly to avoid a repetition of the previous housing crisis.

But as they say, you cannot prevent what you don’t know about, so let’s tackle this one first.

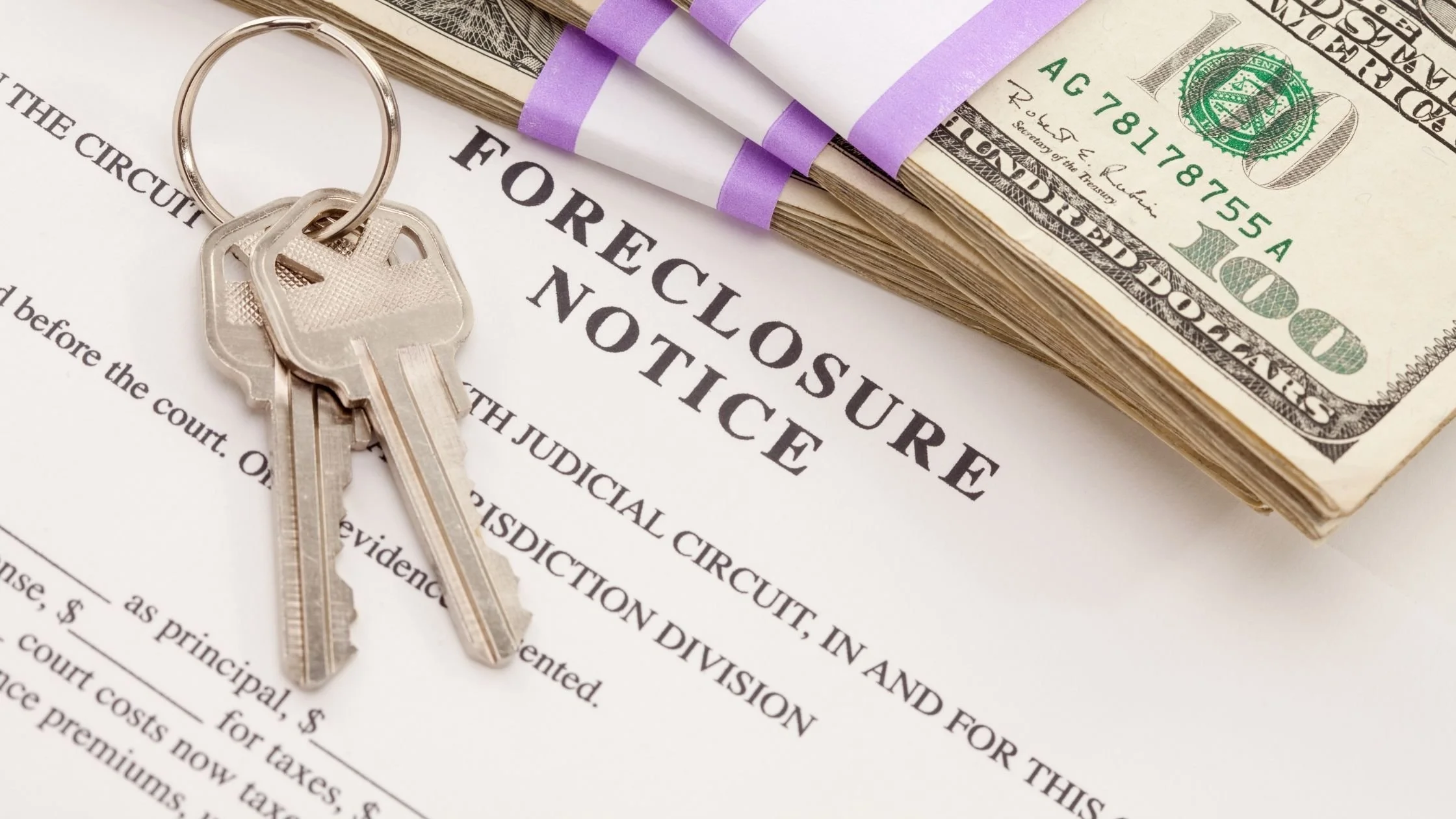

What is Foreclosure?

The legal procedure through which a lender seeks to recoup the amount owing on a defaulted debt by seizing and selling the mortgaged property is known as foreclosure. The default usually occurs when a borrower misses several monthly payments. The most typical reason for foreclosure is missed mortgage payments. However, other acts that violate your mortgage conditions can also lead to foreclosure.

First things first, Call your Lender

For several reasons, homeowners fail to repay their mortgages. There are several causes for this, but the following are the most common:

Divorce

Sudden unemployment

Death in the family

The inability to pay an adjustable interest rate that increases

The best solution for all parties involved is to prevent the foreclosure process altogether, so if you think you won't be able to make a payment, contact your lender right once.

Here are some possible resolutions your lender might consider:

Forbearance: Lenders may be willing to give you some leeway before pursuing legal action. steps to build a budget-friendly payment plan

Repayment Plan: For a certain length of time, this option adds a tiny amount to your existing monthly payments until the amount of the missing payment is recovered.

Note Modification: Your lender may consider changing the loan's terms, such as freezing the interest rate on an adjustable-rate mortgage or extending the loan's term.

Partial Claim: Some government loans can be used to make up for missing mortgage payments, but there are some lending requirements that must be met.

Debt forgiveness: Your lender may forgive or waive this missing payment if you can devise a strategy to bring your debt current after this missed payment. However, keep in mind that this is an uncommon occurrence.

Understanding the Foreclosure Process

Understanding the foreclosure process might help you avoid foreclosure or sell your house more quickly for a reasonable price.

Pre-foreclosure is the stage of the foreclosure process before the lender submits formal documents. This is the best moment to halt a foreclosure because your credit rating will be unaffected at this stage.

When the lender issues a Notice of Default, the foreclosure process begins. This is a public document that shows where the home is situated and that the homeowner is behind on payments, with the possibility of the home being seized. Each state is different in terms of how fast a Notice of Default is submitted. Lenders usually wait 60 days after a missing payment before launching a claim. Lenders must normally wait 90 days after filing before selling or auctioning the property.

Following the 90-day period, a notice is published in the newspaper for up to 20 days, informing the public that the residence may be available for sale or auction. The prior renters must vacate the property once it has been auctioned off unless a rental arrangement has been reached between the new owners and the previous owners.

Now that we’ve discussed the what’s of foreclosure, how can we stop foreclosure?

Ways to Stop a Foreclosure

If your lender refuses to engage with you, you have additional alternatives for stopping the foreclosure process. You must, however, move promptly and thoroughly investigate which choice is best for your case.

Reinstatement

Loan modification

Deed-in-lieu of foreclosure

Short sale

Why is Selling your House a Better Option?

It's worth checking to determine if your property has enough equity to sell and preserve your investment. The difference between what you owe on your house and its market worth, as determined by variables such as price appreciation, is known as equity.

Many homeowners have significantly more equity in their houses than they think in today's real estate market. Buyer demand has been high in recent years, while housing availability has been low.

According to CoreLogic, on average, homeowners gained $33,400 in equity over the last 12 months, and the average equity on mortgaged homes is now $216,000. So what this means for you is that chances are your home’s value has risen dramatically. If the current value of your house is more than the amount you still owe on your loan, you may be able to take advantage of the difference.

But since putting up your home on sale can prove to be a lot of work, and time is of value when it comes to foreclosure. Don’t worry! Ash Creek is here for you to offer an all-cash offer for your home. Close and move out on the date of your choosing. Contact us today!